Single-family housing has historically been an important component of economic growth. Not necessarily because of the actual production of the homes, but because of the ripple effect — or what economists call the multiplier effect. Without going down the rabbit hole of an economic deep dive, the simplest explanation is that when households buy a home they usually buy more than just the physical home.

If you are buying a home, you will probably be buying other things that go with a home. Depending on whether you are a “first time”, “trade up”, “downsizing” or “relocation” homebuyer will determine how many other purchases that you will make along with your house. The other purchases may include landscaping, painting, roof repair/replacement, remodeling, furniture, appliances, accessories and insurance to name a few. The benefit of someone buying a house ripples through those other sectors of the economy and increases sales to their businesses. This is why they call it a multiplier effect since one purchase multiplies into additional purchases.

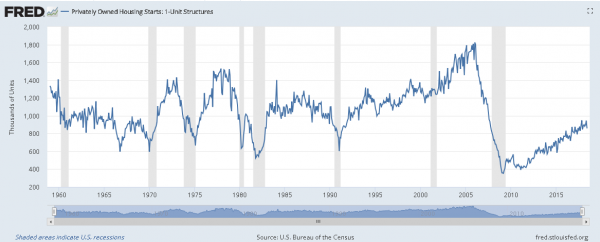

If we want to determine if housing can give us a clue about future economic activity, examining housing data would be a good start. Housing starts for one unit structures are a source of information regarding future home buying activity. The Census Bureau gathers data from the US Department of Housing & Urban Development and generates a monthly report on housing starts.

What is clear, when examining the data, is that each business cycle has had a slightly different pattern, but in five out of the seven business cycles since 1960, there was a clear downtrend in housing starts before the recession began. The picture is virtually the same if you look at data on building permits and new home sales. There is insufficient data to examine existing home sales.

The graph below illustrates the relationship between housing starts and recessions.

A few notes:

-Data collection did not occur for the full business cycle before the 1960 recession so it was not included in the analysis. The limited information (January 1959-August 1960) does show a downtrend before the 1960 recession but does not show where the peak was.

-The business cycle from February 1961 through November 1969 gave a false signal. Housing starts peaked in February 1964, experienced a sustained downturn and then recovered most of the decline by January 1965 before suffering a second downturn that led into the recession that started December 1969.

-The business cycle from March 1991 through March 2001 gave a false signal since housing starts peaked December 1998 but bottomed July 2000 and were in an uptrend when the recession hit March 2001.

-The business cycle from November 1982 through July 1990 has the longest sustained downturn (77 months) before the recession began. The shortest was 6 months.

-For the five cycles when there was a clear downtrend before the recession, the average lag between the peak in housing starts and the start of the recession was 29 months.

All of this leads to the question of what the current data is showing us. Looking at the chart, the current picture for housing starts is the most similar to the March 1991 to March 2001 business cycle. In the current business cycle, it is not clear if a peak has been established. With the drop in housing starts in June 2018, the peak would currently be May 2018 but, one month does not establish a trend. Only the passage of time will tell us whether that is truly the peak, but the picture is clearly similar.

Housing will most likely not be the cause of the next recession and it is very unlikely that the housing market will experience the devastation that occurred in the last recession once the next recession starts. It is a bit sobering to realize that if we are at the peak for housing starts, it is the lowest peak since data has been collected. The flip side is that, if we are going to get closer to previous peaks, then housing starts still have a way to go.

My message is simple:

-Housing is an important component of economic growth;

-Housing starts for one unit structures have a good track record (5 out 7) of establishing a downtrend before a recession starts; and

-Watch housing for any signs of deceleration.

Washington Trust Bank believes that the information used in this study was obtained from reliable sources, but we do not guarantee its accuracy. The views of this article are those of the author and do not necessarily represent the views of management. Neither the information nor any opinion expressed constitutes a solicitation for business or a recommendation of the purchase or sale of securities or commodities.

Steve Scranton is the Chief Investment Officer and Economist for Washington Trust Bank and is a CFA charter holder with over 30 years of investment experience with equities, tax-exempt and taxable fixed income securities. Steve actively participates on committees within the bank to help design strategies and policies related to client and bank owned investments. Steve also serves as the economist for the Bank and has been a featured speaker for both client and professional organization events throughout the Northwest.

![]() Links with this icon are leaving Washington Trust Bank's website. This link is provided as a courtesy. Washington Trust Bank does not endorse or control the content of third party websites.

Links with this icon are leaving Washington Trust Bank's website. This link is provided as a courtesy. Washington Trust Bank does not endorse or control the content of third party websites.

Home | Contact | Locations | Privacy Policy | Terms & Conditions | Safe Act Numbers | Posting Rules

Rates and fees subject to change. Entire contents: Copyright 2014 Washington Trust Bank. An Equal Opportunity Employer.