The second quarter was mostly a quiet one for stocks, here and abroad. While the international developed and emerging markets slightly outperformed domestic stocks, most major stock indices were not able to provide a 1% return during the quarter. As a result, for the first half of the year, the S&P 500 has only managed a 1.2% gain. International equities (as measured by the MSCI EAFE Index), because of their strong first quarter, have provided a year-to-date return of 5.88%. Oil prices firmed during the quarter, which helped commodities return over 4.5%, reversing their negative trend. In contrast, REITS, which have had a very strong run, reversed their trend and declined 9%.

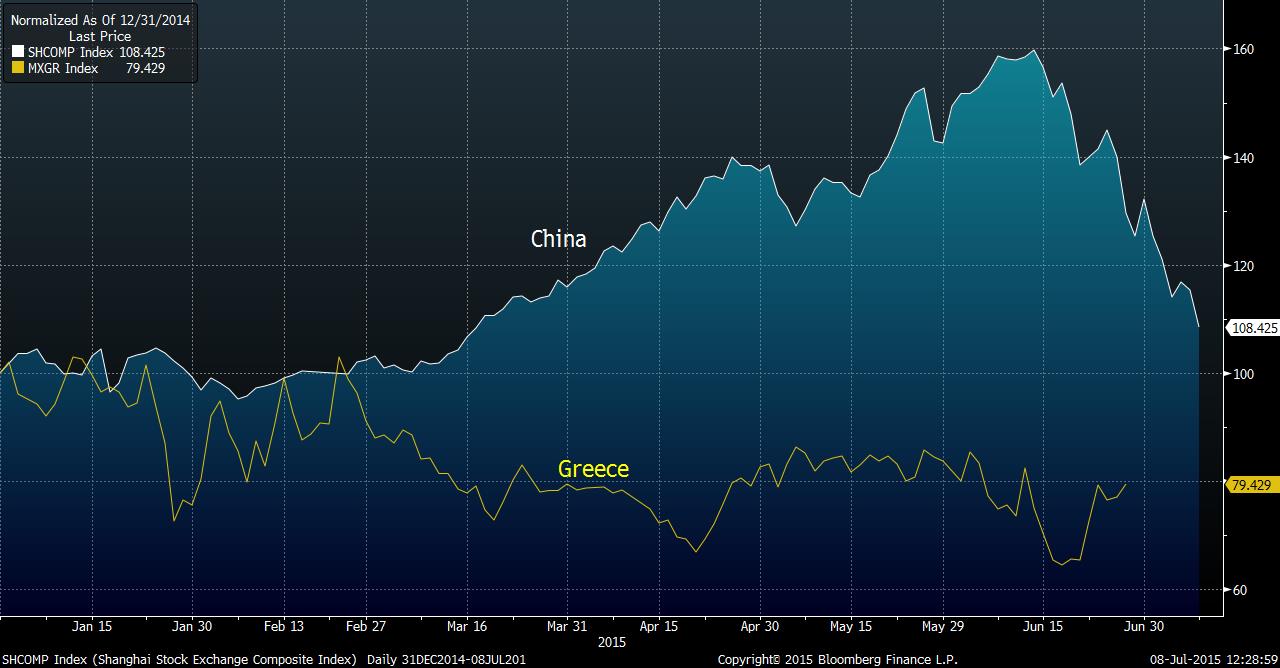

While most major stock indices were pretty quiet, Greek and Chinese stocks were anything but. After failing to reach an agreement with creditors, Greece’s financial crisis entered a new phase. The uncertainty of Greece remaining in the Euro has increased, which helped Greek stocks lose almost 10%. This drop does not sound like much given the extent of the crisis, but Greek stocks are off 25% for the year and a total of over 80% for the last five years. While Greece’s economy is small relative to other developed markets, its troubles have had an outsized effect on equity markets and we expect that this will continue.

China’s stock market, on the other hand, surged until plunging over 20% in the second half of June. At their peak, Chinese stocks were up over 150% during the least twelve months. This incredible rise came despite China’s economic slowdown. In fact, before this run up, China’s stock market had seen very little movement for several years. The reason Chinese stocks did so well had less to do with the economy and more to do with the People’s Bank of China’s involvement. Because of the Bank’s liberalization, the markets have seen a rush of new Chinese investors, leverage has soared, and corporations have shut down activities and diverted capital into the stock market. Although Chinese stocks have declined 20%, the coming weeks should give us a better indication of whether this truly is a bear market for China or if this is simply a dramatic correction.

(Bloomberg)

Back at home, corporate earnings managed to grow 2.2% during the first quarter. However, for the second quarter, S&P 500 earnings are expected to decline by 3%. Once earnings are released, we shall see if a profit recession for U.S. companies is a potential reality.

With the U.S. economy seemingly improving from its poor first quarter, expectations of a Fed rate increase grew. In anticipation, bond yields all along the curve rose. The yield on the ten year Treasury jumped about a half a point to end the quarter yielding 2.35%. Bonds with long maturities were hurt the most by the rise in rates with bonds maturing in 25 years or more, returning a -9.43%.

If the economy continues to move in its current direction, we would expect the Fed to raise rates a quarter of a point in either September or October later this year.

Given the market’s anticipation of a rate increase, the uncertainties in Greece and China, the weakness in the economies of much of the developed world, and the potential for corporate profit declines, the rest of the year could prove to be quite adventurous for investors. To use the often-misquoted Bette Davis line from All About Eve, “Fasten your seat belts, it’s going to be a bumpy night.” She actually did not say ride.

Washington Trust Bank believes that the information used in this study was obtained from reliable sources, but we do not guarantee its accuracy. Neither the information nor any opinion expressed constitutes a solicitation for business or a recommendation of the purchase or sale of securities or commodities.

Washington Trust Bank.

![]() Links with this icon are leaving Washington Trust Bank's website. This link is provided as a courtesy. Washington Trust Bank does not endorse or control the content of third party websites.

Links with this icon are leaving Washington Trust Bank's website. This link is provided as a courtesy. Washington Trust Bank does not endorse or control the content of third party websites.

Home | Contact | Locations | Privacy Policy | Terms & Conditions | Safe Act Numbers | Posting Rules

Rates and fees subject to change. Entire contents: Copyright 2014 Washington Trust Bank. An Equal Opportunity Employer.