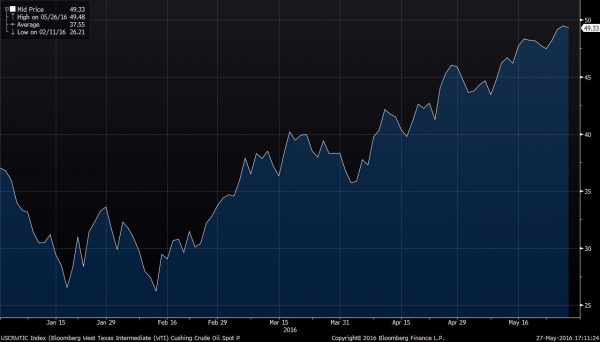

Oil prices have been on a roller coaster ride as of late. From a high of $107/barrel in July 2014, oil dropped to a low of $26/barrel this February. Since that time, oil has moved back to $50/barrel. Prices began to decline after a November 2014 OPEC meeting in which Saudi Arabia declared that markets would determine the price. In other words, members would stop cooperating on supply and instead compete for market share. As a result, the supply of oil increased beyond the demand – to the tune of 1.4 million barrels per day.

Since that time any attempts to agree on cuts have failed, including the latest meeting in Doha this April that produced open sparring between Russia and Saudi Arabia instead of an agreement.

Despite this, oil has risen pretty quickly. A move to $50 a barrel may seem insignificant compared to oil’s 2014 prices, but the move is a 90% increase off the lows – and that is significant. While demand has kept pace, the change in equilibrium stems from supply disruptions. Canadian wildfires have forced temporary closures costing about 1 million barrels per day. Militant attacks in Nigeria have caused production losses of around 800,000 barrels per day. These two disruptions alone more than offset the 1.4 million barrels per day in oversupply – and I haven’t added production declines in Kuwait, Iraq, Venezuela, and the US. Therefore, the culprit behind the price rise is the dip in supply.

Most of this dip is short term, however, and production will resume. So, what are the long-term prospects for oil?

As I mentioned in a previous blog (click here), Saudi Arabia has geopolitical incentives to keep prices down – namely its clash with Russia and Iran. Putin’s military involvement in Syria, beginning last September, changed the conflict considerably. At that time, Syria’s government teetered on collapse; but Russia’s attacks on opposition forces, many of them supported by Saudi Arabia, turned the tide against the rebels and have entrenched the Assad regime. Before the ceasefire, Russia was spending between $5 million and $8 million per day on air strikes, so the incursion has not been cheap. Renewed fighting in Aleppo has ended the fragile ceasefire and once again Saudi Arabian-backed Sunni rebels are in open military conflict with Russia and Iran. Besides the military conflict, Russia seems to be pursuing an economic conflict as well. Instead of cooperation on supply, Russia has promised to ramp up production to 12-13 million barrels per day from its current 10.91 million. Russian production is already at a 30 year high.

And that brings us to the other combatant – Iran. Since the US lifted sanctions, Iran has increased production significantly, and although it may take years for Iran to completely restore capacity, output could climb to 1 million barrels per day by year’s end. Iran has made it clear that it has no intention to agree to any production cut until it regains market share and plans to produce 4 million barrels per day.

What has been the response from Riyadh? Recently Saudi Aramco CEO Nasser said, “We’re seeing global increase in demand. We are meeting that call on us.” And Saudi Arabia’s recent announcement to diversify away from oil is telling the world that, long term, it is not going to be dependent on high priced oil. As the low cost producer, Saudi Arabia intends to outlast its rivals. So don’t expect the short-term supply shortage to last. And if you think economics will trump geopolitics in the near-term – think again. Saudi Arabia is concerned about the military and diplomatic advances Tehran has made recently, including the nuclear agreement and subsequent lifting of sanctions. Closer ties between Iran and the US are a major concern, as well as combating a “Shia Crescent” in the Middle East. Saudi Arabia’s present military build-up puts its budget behind only the US and China. Riyadh is even outspending Russia.

Besides this geopolitical rivalry, there could be a new “swing player” in the market keeping prices low – the US. Until recently US production had been very resilient, but as a result of budget cuts, domestic producers have more than 6,500 wells drilled but not completed. If oil trades between $50 and $60, many of these wells could become profitable. Platts Analytics believes that Texas alone could produce 1.25 million barrels per day in about 30 days. That ability to quickly bring large quantities of oil to market could put a lid on prices. So, while predicting the future of oil is precarious, we don’t see prices rising to their 2014 levels any time soon.

Washington Trust Bank believes that the information used in this study was obtained from reliable sources, but we do not guarantee its accuracy. Neither the information nor any opinion expressed constitutes a solicitation for business or a recommendation of the purchase or sale of securities or commodities.

Washington Trust Bank.

![]() Links with this icon are leaving Washington Trust Bank's website. This link is provided as a courtesy. Washington Trust Bank does not endorse or control the content of third party websites.

Links with this icon are leaving Washington Trust Bank's website. This link is provided as a courtesy. Washington Trust Bank does not endorse or control the content of third party websites.

Home | Contact | Locations | Privacy Policy | Terms & Conditions | Safe Act Numbers | Posting Rules

Rates and fees subject to change. Entire contents: Copyright 2014 Washington Trust Bank. An Equal Opportunity Employer.