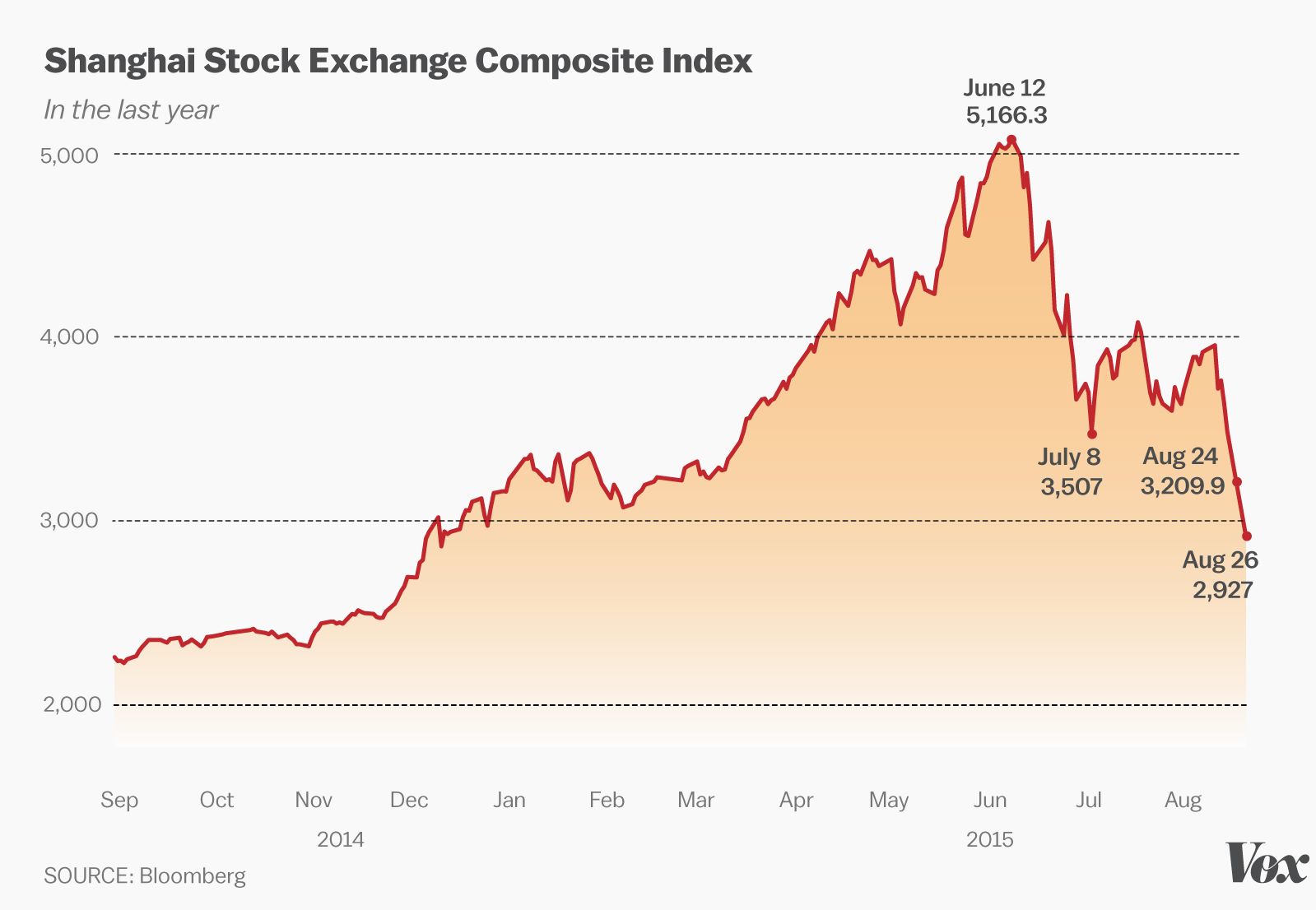

China has made the news in recent months because of the roller coaster ride of its equities, its slowing growth, and the effects China has had on global markets. The latest official GDP numbers from China show growth slowed to 6.9%, below the government’s target of 7%. That target has since been lowered to 6% from 7%.

Economic growth in China has long been founded on high levels of savings and investment, growth of manufacturing and exports, and the migration of low-productivity rural workers to higher-productivity urban jobs. These trends are no longer sustainable, and as a result growth is slowing.

China has transformed very quickly to the world’s second largest economy. That growth surge was built on a simple truth: Chinese wages were far below Western wages, and therefore the Chinese were able to produce low tech products at lower cost than possible in the West. Since Chinese workers were unable to purchase many of the products they made, given their low wages, China built its economy on exports.

However, for export growth to continue, China would have to maintain its wage differential. Unfortunately for China, that differential in many respects has gone. The ability of China to maintain a rapidly growing economy in the long run depends largely on the ability of the Chinese government to implement comprehensive economic reforms to rebalance the Chinese economy and make consumer demand the main engine of economic growth.

The question is whether the Communist Party can maintain political order as the economy shifts. To move from an economic model premised on the planned suppression of private household consumption (by maintaining artificially low wages and input costs) to one grounded in the expansion of domestic consumption, China’s leaders are pushing through a set of reforms to rebuild the fiscal foundations of local governments around new local taxes and municipal bond sales rather than land sales.

Continuing that process of transformation from a state-run economy to consumer-driven capitalism poses challenges for both future growth and the Communist Party. Rapid gains in productivity are easier to achieve in manufacturing than services. But the double-digit growth that propelled such prosperity can’t be maintained as services become a larger share of the economy.

Chinese leadership, which is always concerned about stability, has acknowledged the necessity of economic deceleration and is orienting its companies and citizens for slower growth. The shift to services is part of a planned process. The reward for slower income growth is better for environmental quality and an improved social safety net. This shift also underpins a more vibrant middle class that is an increasing source of strength. But this growing middle class has aspirations not dissimilar to ours: to have a nice home, a car and college education for their children.

The process of change is not going to be easy for China and the unknowns will increase market anxiety. Because today’s capital markets are more intertwined than ever, even though the US economy is not significantly dependent on China, any anxiety felt in China will spread to our equity markets – at least temporarily.

Washington Trust Bank believes that the information used in this study was obtained from reliable sources, but we do not guarantee its accuracy. Neither the information nor any opinion expressed constitutes a solicitation for business or a recommendation of the purchase or sale of securities or commodities.

Washington Trust Bank.

![]() Links with this icon are leaving Washington Trust Bank's website. This link is provided as a courtesy. Washington Trust Bank does not endorse or control the content of third party websites.

Links with this icon are leaving Washington Trust Bank's website. This link is provided as a courtesy. Washington Trust Bank does not endorse or control the content of third party websites.

Home | Contact | Locations | Privacy Policy | Terms & Conditions | Safe Act Numbers | Posting Rules

Rates and fees subject to change. Entire contents: Copyright 2014 Washington Trust Bank. An Equal Opportunity Employer.